How I Synced My Health Insurance with My Investment Rhythm — A Real Talk

What if your health insurance wasn’t just a safety net, but part of your investment strategy? I used to treat it as a monthly bill—until a close call changed everything. Now, I see it differently: not as an expense, but as a rhythm keeper. It protects my capital, stabilizes my decisions, and keeps my long-term investments on track. This is how I learned to align risk protection with financial growth—without overcomplicating things or breaking the bank. What began as a reluctant monthly payment became a cornerstone of financial discipline, one that quietly supports every dollar I invest. This is not about fear or worst-case scenarios. It’s about clarity, control, and consistency—the real foundations of lasting wealth.

The Wake-Up Call: When Health Risk Hit My Wallet

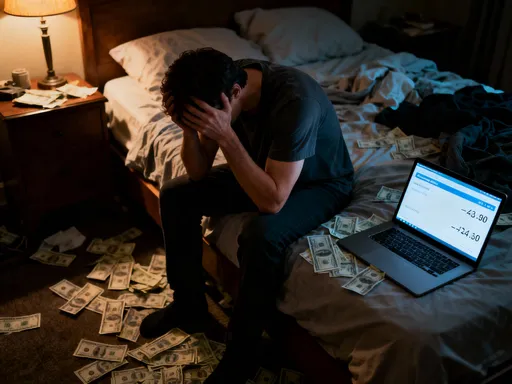

For years, I believed I was invincible—or at least financially bulletproof. I was in my early thirties, working steadily, contributing to a 401(k), and watching my index funds climb. I had an emergency fund, a modest home, and what I thought was a solid financial foundation. But I had skipped one critical piece: comprehensive health insurance. I had a basic employer plan, yes, but I hadn’t reviewed it in years. I assumed it would cover me if something went wrong. Then, one winter, I developed severe abdominal pain that landed me in the emergency room. What followed was a week-long hospital stay, a diagnosis of acute pancreatitis, and a medical bill that totaled over $28,000 after insurance. My plan had high deductibles and limited out-of-network coverage, and the specialist who treated me wasn’t fully in-network. I ended up paying nearly $12,000 out of pocket—more than half of my emergency savings. That moment was a financial earthquake. I wasn’t just shaken; I was exposed. The money I had planned to use for a home renovation—funds I had mentally earmarked for long-term wealth building—was gone in weeks. Worse, the stress forced me to pause my investment contributions for three months while I rebuilt my cash reserves. I realized then that risk wasn’t just a theoretical concept. It was real, immediate, and it didn’t care about my investment timeline. That single health event didn’t just affect my health—it disrupted my entire financial rhythm. I had been investing wisely, but I hadn’t protected wisely. And without protection, even the most disciplined investment strategy can unravel overnight.

This experience didn’t just change my attitude toward health insurance; it changed how I viewed all financial planning. I began to see risk management not as a separate category, but as the foundation of wealth building. Every dollar I invest assumes a certain level of stability—stability in income, in health, in daily life. When that stability is compromised, the entire structure becomes vulnerable. I had assumed that as long as I was young and healthy, I could delay optimizing my coverage. But health risks don’t follow a schedule. They don’t wait until you’ve saved enough or paid off your mortgage. They strike when they strike. And if you’re not prepared, the financial fallout can erase years of progress. I learned that insurance isn’t about predicting the future—it’s about preserving the future you’re working so hard to build. From that point on, I stopped seeing health insurance as a cost and started seeing it as a safeguard for my capital. It wasn’t just about covering medical bills; it was about ensuring that my investment journey could continue, uninterrupted, no matter what life threw my way.

Health Insurance as a Financial Anchor, Not Just a Cost

Before my hospitalization, I viewed health insurance premiums the way most people do—as a necessary evil, a monthly drain on cash flow with no visible return. I paid them grudgingly, like a tax I couldn’t avoid. But after the financial shock of my medical crisis, I began to see them differently. I started to think of premiums not as an expense, but as a form of financial insurance for my investment strategy. Just as shock absorbers protect a car from damage on rough roads, health insurance protects your financial plan from sudden, jarring disruptions. It doesn’t generate returns like a stock or bond, but it prevents catastrophic losses that could derail decades of disciplined saving and investing. This shift in perspective was subtle but transformative. Instead of resenting the premium, I began to appreciate it as a small, predictable cost that bought me something far more valuable: peace of mind and financial continuity.

One of the most powerful benefits of proper health coverage is that it prevents forced liquidation of assets. Without insurance, a major medical event could force you to sell investments at the worst possible time—perhaps during a market downturn, locking in losses and undermining years of compound growth. I’ve seen it happen to others: a friend had to cash out a portion of her retirement account to cover surgery costs, losing both the long-term growth potential and facing early withdrawal penalties. Another acquaintance sold stocks to pay for a family member’s treatment, only to watch those same stocks double in value within a year. These aren’t just hypotheticals—they’re real financial setbacks that could have been avoided with better protection. By maintaining a strong health insurance plan, I ensure that unexpected medical costs don’t force me to make desperate financial decisions. My portfolio stays intact, my contributions continue, and my long-term goals remain on track. This is not just about avoiding debt; it’s about preserving the momentum of wealth accumulation. Every dollar I don’t have to spend on an emergency medical bill is a dollar that can stay invested, compounding over time. In that sense, health insurance isn’t a cost—it’s a compound growth enabler.

Moreover, having reliable coverage reduces decision fatigue during crises. When you’re dealing with a health scare, the last thing you should be worrying about is whether you can afford treatment. With a solid plan in place, I can focus on recovery, not bills. This emotional stability translates into better financial decision-making. I’m not pressured to cut corners, delay care, or choose cheaper providers that might not offer the best outcomes. I can make medical decisions based on health, not cost. And that, in turn, supports faster recovery and a quicker return to work and normal income flow. The ripple effects are profound: shorter recovery times mean less lost income, which means less strain on my budget and more consistency in my investment habits. In this way, health insurance doesn’t just protect my body—it protects my earning potential, my cash flow, and my ability to stay financially disciplined. It’s not an isolated expense; it’s a strategic component of a resilient financial life.

Matching Coverage to Life Stages and Investment Goals

One of the biggest mistakes I made early on was treating health insurance as a one-size-fits-all solution. I assumed that once I had a plan, I could set it and forget it. But just as my investment strategy has evolved over the years—from aggressive growth in my thirties to more balanced allocation in my forties—so too has my approach to health coverage. Life stages bring different risks, responsibilities, and financial priorities, and your insurance should reflect that. In my twenties, I was single, childless, and focused on building wealth. I opted for a high-deductible health plan with an HSA because the lower premiums freed up cash for investing, and the tax advantages aligned with my long-term goals. I accepted the higher out-of-pocket risk because I was healthy and could afford to pay for minor medical expenses if needed. That strategy worked well for that phase of life.

But everything changed when I bought a home and started a family. Suddenly, my financial landscape shifted. I had a mortgage, a growing child, and a tighter budget. The risk of a major medical event wasn’t just personal anymore—it could affect my entire household. I realized that a high-deductible plan, while still tax-efficient, might not provide enough immediate protection if my child needed urgent care or if my spouse faced a complication during pregnancy. I switched to a PPO plan with a moderate deductible, broader network access, and better coverage for preventive care and pediatric services. The premiums were higher, but the peace of mind was worth it. I wasn’t just protecting my income anymore—I was protecting my family’s stability. This new plan ensured that we could see specialists without referrals, access top-tier hospitals, and avoid surprise bills that could strain our monthly cash flow. It also allowed me to maintain consistent investing, knowing that a medical emergency wouldn’t force us to dip into our college fund or home equity.

Now, in my mid-forties, I’ve adopted a hybrid approach. I still prioritize an HSA-eligible plan because of the triple tax advantage—contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. But I’ve increased my contribution level and built a dedicated medical savings account within my HSA, investing a portion of the funds for long-term growth. This allows me to use the HSA not just as insurance, but as a stealth retirement vehicle. I pay current medical expenses out of pocket when possible and let the HSA balance grow, knowing I can reimburse myself tax-free in retirement. This strategy aligns perfectly with my investment rhythm: I’m still growing wealth, but I’m also preparing for higher healthcare costs in later years. The key lesson is that health insurance isn’t static. It should evolve alongside your life and financial goals, just like your portfolio. Regular reviews—ideally every year during open enrollment—are essential to ensure your coverage remains in sync with your current reality and future aspirations.

The Hidden Link Between Premiums and Portfolio Discipline

One of the most unexpected benefits I’ve discovered is how paying health insurance premiums has strengthened my overall financial discipline. At first glance, a monthly premium seems like a fixed cost with no return—something to be minimized or avoided. But over time, I’ve come to see it as a behavioral anchor, a non-negotiable commitment that reinforces good money habits. Just like my automatic 401(k) contribution, my premium payment is set up to deduct automatically from my account. This consistency creates a rhythm, a financial routine that makes it easier to stick to other long-term goals. Knowing that a certain amount is going toward protection each month forces me to budget more carefully, avoid lifestyle inflation, and prioritize essential spending. It’s a small but powerful form of financial training.

This fixed obligation has also made me more intentional about discretionary spending. When I see that $450 is leaving my account every month for insurance, I’m less likely to justify impulse purchases or unnecessary subscriptions. I think more critically about value, trade-offs, and long-term consequences. This mindset extends to my investing behavior. Because I’ve conditioned myself to treat premiums as untouchable, I’m more likely to do the same with my investment contributions. I don’t view them as optional extras; I treat them as essential line items, just like rent or utilities. This mental framing has been crucial in maintaining consistency, especially during market downturns or periods of personal stress. When others might pause contributions out of fear or uncertainty, I keep going—because stopping feels like breaking a promise to my future self.

Moreover, the predictability of premiums helps me plan my cash flow more effectively. I know exactly how much I need to set aside each month, which reduces financial anxiety and improves my ability to forecast expenses. This clarity allows me to allocate surplus income more confidently toward investments, knowing that my protection costs are already accounted for. It’s a subtle but powerful form of financial alignment: by securing the downside, I create more space to focus on the upside. The premium isn’t just buying medical coverage; it’s buying discipline, structure, and confidence. It’s a small price to pay for the stability that allows my investments to grow steadily, year after year, without interruption.

Choosing Plans That Complement, Not Compete With, Investments

Not all health plans are created equal when it comes to financial synergy. I’ve learned that the best plan isn’t necessarily the cheapest or the most comprehensive—it’s the one that fits seamlessly into your overall financial strategy. Early on, I made the mistake of choosing a plan based solely on premium cost, only to discover later that high out-of-pocket expenses could still drain my savings. Then I swung the other way, opting for a premium gold-tier plan with low deductibles and extensive coverage. It felt safe, but the monthly cost was so high that it ate into my ability to invest. I was over-insuring at the expense of wealth building—a trade-off I didn’t fully understand at the time. The real goal isn’t to minimize premiums or maximize coverage; it’s to find a balance where protection supports, rather than competes with, your investment goals.

What I now prioritize is flexibility, network access, and long-term tax efficiency. An HSA-eligible high-deductible health plan has become my preferred choice because it offers all three. The higher deductible means lower premiums, freeing up cash for investing. The HSA provides a powerful tax-advantaged account that can be used for current medical expenses or saved and invested for future healthcare costs in retirement. I contribute the maximum allowed each year, treating it as a supplemental retirement account. The funds grow tax-free, and if I don’t need to use them for medical expenses, I can withdraw them after age 65 for any purpose, paying only income tax—similar to a traditional IRA. This dual-purpose nature makes the HSA one of the most efficient financial tools available. It’s not just insurance; it’s a stealth wealth-building vehicle.

Equally important is network flexibility. I’ve learned the hard way that even with good coverage, out-of-network care can lead to surprise bills that insurance doesn’t fully cover. I now choose plans with broad provider networks, especially in my region, so I can access quality care without financial risk. I also look for plans that cover preventive services at 100%, because staying healthy is the best way to avoid high medical costs down the road. Preventive care—annual checkups, screenings, vaccinations—helps catch issues early, when they’re easier and cheaper to treat. This proactive approach reduces long-term risk and supports financial stability. By choosing a plan that aligns with both my health needs and financial goals, I ensure that my protection strategy enhances, rather than hinders, my investment rhythm. It’s not about spending more or less—it’s about spending wisely, so every dollar serves a purpose.

Avoiding the Trap: Over-Insuring or Under-Protecting

Finding the right level of coverage is one of the most delicate balancing acts in financial planning. I’ve been on both sides of the spectrum, and both come with serious risks. Early in my career, I under-protected, assuming I wouldn’t need much coverage. That decision nearly cost me everything. Later, during a period of higher income, I over-insured, paying for a premium plan with benefits I rarely used. I was paying thousands extra each year for coverage I didn’t need—money that could have been invested in low-cost index funds and compounded over time. Both extremes undermined my financial goals. Under-protecting exposed me to catastrophic risk; over-insuring slowed my wealth accumulation. The key is finding the sweet spot: enough coverage to protect your assets, but not so much that it drains your ability to grow them.

One framework I now use is to assess coverage based on my current risk exposure and financial capacity. I ask myself: What would happen if I faced a major medical event today? Could I cover the out-of-pocket costs without selling investments or going into debt? If the answer is no, I need more protection. But if I’m paying for benefits I’ll almost certainly never use—like unlimited specialist visits or private hospital rooms—I’m likely overpaying. I also consider my income stability. During freelance or self-employed periods, when income is less predictable, I lean toward plans with moderate premiums and solid out-of-network coverage, even if deductibles are higher. When employed full-time with employer subsidies, I maximize HSA contributions and choose plans that offer the best tax advantages. I review my coverage annually, adjusting as my life changes. This disciplined approach helps me avoid emotional decisions and stay focused on long-term financial health.

Red flags I watch for include rapidly increasing premiums with no added value, limited provider networks that restrict care options, and plans that don’t cover essential services I actually use. I also avoid plans that create false security—those that seem comprehensive but have hidden exclusions or high co-pays for common procedures. Transparency is crucial. I read the summary of benefits carefully, ask questions, and compare options side by side. The goal isn’t perfection—it’s adequacy. I don’t need the best plan on the market; I need the right plan for my life right now. By staying vigilant and intentional, I ensure that my health insurance remains a supportive force in my financial life, not a burden or a blind spot.

Building a Financial Rhythm: Where Protection Meets Growth

Today, health insurance isn’t a separate line item on my budget—it’s woven into the fabric of my financial strategy. I treat it with the same seriousness as my Roth IRA contribution or my monthly investment transfer. It’s non-negotiable, automatic, and aligned with my long-term vision. This integration has created a powerful rhythm: grow steadily, protect wisely, repeat. I invest in low-cost index funds for long-term growth, contribute to my HSA for tax-advantaged protection, and maintain a balanced plan that covers my family’s needs without overextending my budget. Each piece supports the others, creating a system that’s greater than the sum of its parts. I no longer see risk management and wealth building as competing priorities. They are two sides of the same coin—both essential for lasting financial confidence.

This rhythm has given me something priceless: peace of mind. I no longer lie awake wondering what would happen if I got sick. I know my coverage is strong, my savings are protected, and my investments are safe from forced liquidation. That mental clarity allows me to stay focused on my goals, even during market volatility. I don’t panic when stocks dip because I know my foundation is secure. I can afford to be patient, to let compounding work its magic over time. And that patience is where real wealth is built—not in chasing returns, but in consistent, disciplined action, protected from avoidable setbacks.

Looking back, I realize that my journey wasn’t just about finding the right insurance plan. It was about redefining what financial security means. It’s not just about how much you earn or how much you invest. It’s about how well you protect what you have, so you can keep growing it, year after year. Health insurance, once an afterthought, has become a cornerstone of that security. It’s not glamorous, but it’s essential. It’s the quiet force that keeps my financial life on track, allowing me to invest with confidence, live with intention, and plan for a future that’s not just wealthy, but truly resilient.